Insider threat prevention in accounting is the practice of deploying targeted controls to protect sensitive financial data from risks that originate inside your own organization. Over one-third of data breaches in financial services trace directly to insider-related causes, making this the most underestimated exposure in accounting operations. Regulatory bodies including the Wolfsberg Group and the Bank for International Settlements now expect firms to treat insider risk as a formal compliance obligation, not an HR footnote. The most effective defense combines behavioral analytics, anti-money laundering transaction monitoring, and continuous access governance into a single, integrated program.

What are the main types of insider threats in accounting?

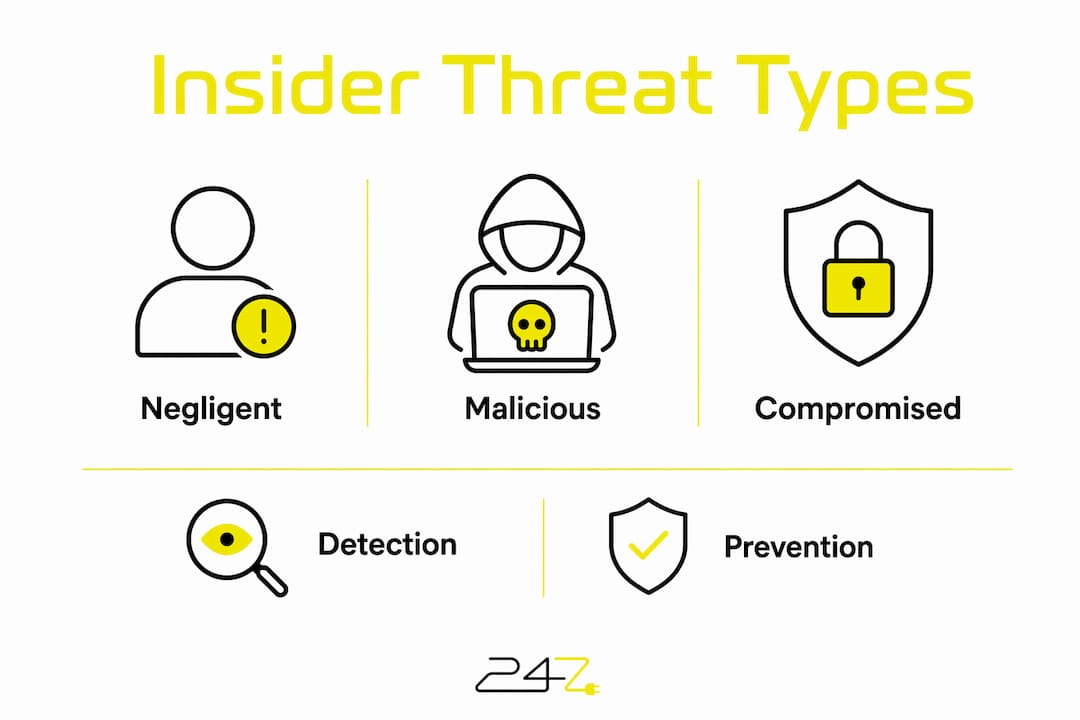

Accounting environments face three distinct insider threat categories, and each requires a different detection approach. Treating them as a single problem is the fastest way to miss the one that actually hits you.

Negligent insiders are the most common category. Negligent employees cause 58% of all insider-related security incidents. That figure reflects mistakes, poor password hygiene, and failure to follow data handling policies rather than malicious intent. The damage is real regardless of intent.

Malicious insiders act with purpose. They include employees who steal client data before resigning, accountants who manipulate journal entries to cover embezzlement, or finance staff who sell access credentials to external fraud rings. These actors are harder to detect because their access is legitimate. The threat only becomes visible through behavioral deviation, not perimeter alerts.

Compromised insiders represent a third category that accounting teams frequently overlook. An external attacker gains control of a legitimate employee account through phishing or credential theft, then operates inside the network with full authorized access. From a system perspective, the activity looks normal. Detection requires behavioral baselines, not just access logs.

Third-party and vendor risks compound all three categories. Accounting departments routinely grant ERP access to external auditors, payroll processors, and software vendors. Each connection extends the insider risk surface beyond your direct workforce.

Common insider threat scenarios in accounting include:

- Unauthorized export of client financial records before termination

- Manipulation of accounts payable entries to redirect payments

- Credential sharing between accounting staff to bypass approval workflows

- Vendor account misuse to access billing and contract data

- Sabotage of financial reporting systems during disputes

Pro Tip: Watch for subtle behavioral shifts such as a staff member accessing files outside their normal role scope, downloading large data sets late at night, or requesting access to systems they have never used before. These deviations are early signals, not proof, but they warrant investigation.

How can AML systems detect insider fraud in accounting?

Financial institutions can reconfigure existing AML transaction monitoring systems to track internal user activity, not just external transaction flows. This is one of the most cost-efficient moves an accounting security program can make. The infrastructure already exists. The investment is in reconfiguration and alert workflow design.

Standard AML systems flag unusual transaction patterns for customer-facing activity. Extending those same rule sets to internal user behavior means you can detect an accountant who approves an unusually large wire transfer outside normal hours, or a payroll administrator who modifies direct deposit details for multiple employees in a single session.

The table below shows how standard AML detection scenarios map to internal insider fraud use cases:

| AML Detection Scenario | Insider Fraud Equivalent |

|---|---|

| Unusual transaction velocity | High-volume journal entry modifications by a single user |

| Transactions outside business hours | System access and data exports at 2:00 AM |

| Structuring below reporting thresholds | Repeated small payment approvals to a single vendor |

| Geographic anomalies | Login from an unexpected IP or location |

| Dormant account activity | Reactivated user credentials after offboarding |

Reconfiguring AML workflows for insider detection requires three specific steps:

- Map internal user roles to transaction types. Define what normal activity looks like for each accounting role, including volume, timing, and system access patterns.

- Create insider-specific alert rules. Build rule sets that flag deviations from those baselines, such as access to financial data outside assigned responsibilities.

- Integrate alerts with case management. Route insider alerts to a joint team that includes compliance, HR, and IT, not just the security operations center.

Pro Tip: Combining AML transaction signals with behavioral analytics from identity governance platforms produces far fewer false positives. A single anomaly is noise. The same anomaly paired with a recent performance review flag or an access request outside normal patterns becomes a credible signal.

How does segregation of duties protect accounting systems?

Segregation of duties is critical for SOX compliance and requires continuous monitoring rather than point-in-time reviews. The principle is straightforward: no single employee should control an entire financial process from initiation to approval to recording. In practice, most accounting teams implement SoD at onboarding and then rarely revisit it.

The real risk is accumulated access. An accountant hired for accounts payable gains additional ERP permissions over time as their role expands. Three years later, that person can create vendors, approve invoices, and release payments without a second approver. Traditional role-based SoD checks fail to capture this cumulative exposure across ERP systems and third-party applications.

| SoD Approach | Coverage | Audit Readiness |

|---|---|---|

| Periodic manual review | Point-in-time only | Low, gaps between reviews |

| Continuous automated monitoring | Real-time across all systems | High, evidence captured automatically |

| Pre-provisioning simulation | Conflict prevention before access granted | Highest, prevents issues before they occur |

Modern SoD programs use pre-provisioning simulation to evaluate whether a proposed access grant would create a conflict before it is approved. This shifts the control from reactive to preventive. Pair that with continuous cross-system monitoring across your ERP, accounts payable platform, and payroll system, and you close the gaps that periodic audits miss entirely.

Pro Tip: Configure your identity governance platform to capture timestamped evidence of every access decision and SoD conflict resolution. Auditors under SOX require this trail, and having it automated removes the manual burden from your compliance team.

Why does cross-functional governance matter for insider risk?

Purely IT or HR approaches miss subtle insider risk signals. Effective insider threat prevention in financial environments requires a governance model that connects HR, security operations, compliance, and finance leadership into a single escalation structure. Each function holds a piece of the picture that the others cannot see alone.

HR knows when an employee receives a poor performance review, files a grievance, or announces resignation. Security knows when that same employee starts accessing files outside their normal scope. Finance knows when reconciliation exceptions appear in that employee’s accounts. Blending behavioral analytics with HR-generated intelligence and access governance data produces a risk picture that no single team can assemble independently.

Insider threats also connect to broader financial crime. Insider access enables sanctions evasion, bribery schemes, and money laundering in ways that external controls cannot catch. This means your financial crime compliance framework needs to include insider threat scenarios explicitly, not treat them as a separate IT security problem.

Key governance practices that accounting leaders should implement:

- Establish a joint insider threat working group with representatives from HR, legal, IT security, and finance

- Define escalation protocols that specify when behavioral alerts trigger HR involvement versus legal review

- Conduct quarterly cross-functional case reviews to identify patterns across departments

- Include insider threat scenarios in enterprise fraud resilience testing, not just external attack simulations

- Build anonymized reporting channels so staff can flag suspicious behavior without fear of retaliation

Pro Tip: A speak-up culture is a detection tool. Employees closest to the work often notice irregularities before any system does. Anonymous reporting channels with clear follow-up processes increase the likelihood that those observations reach the right people.

What steps prevent insider threats in accounting teams?

Practical insider threat prevention for accounting requires specific policy decisions, not general security awareness. Finance-specific incident response exercises that simulate payroll outages or wire fraud scenarios build the muscle memory your team needs when an actual incident occurs.

- Enforce least privilege access. Every accounting role should have access to exactly what the job requires, nothing more. Review access quarterly and remove permissions that are no longer needed.

- Automate offboarding. Terminated employee accounts must be disabled within hours, not days. Delayed offboarding is one of the most common and preventable insider risk vectors in accounting.

- Deploy phishing-resistant MFA. MFA deployment is strongly recommended by the FFIEC and directly reduces credential misuse, a primary vector for both compromised insider and malicious insider incidents.

- Require role-specific security training. Generic annual security awareness training does not address the specific risks that accounting staff face. Train your team on recognizing phishing attempts targeting financial credentials and on proper data handling for sensitive financial records.

- Govern third-party vendor access. Every external vendor with ERP or accounting system access should operate under a formal access agreement with defined scope, duration, and review cycles.

“Insider incidents carry longer dwell times and higher per-event losses than external fraud. The financial damage compounds every month detection is delayed. Speed of detection is the single most important variable in limiting that damage.”

Include a finance-specific incident response plan that covers wire fraud reversals, payroll system compromise, and unauthorized data exports. Test it with a tabletop exercise at least once per year, using scenarios drawn from accounting cybersecurity risks your team is most likely to face.

Key Takeaways

Effective insider threat prevention in accounting requires continuous monitoring, cross-functional governance, and access controls that adapt to how accounting roles actually evolve over time.

| Point | Details |

|---|---|

| Negligent insiders dominate | 58% of insider incidents stem from mistakes, not malice, so training and process controls matter most. |

| Extend AML for internal detection | Reconfigure existing transaction monitoring to flag internal user behavior deviations, not just customer activity. |

| Continuous SoD monitoring is required | Periodic access reviews miss accumulated privilege risks; automated real-time monitoring closes that gap. |

| Cross-functional governance is non-negotiable | HR, security, compliance, and finance must share data and escalation protocols to catch insider signals early. |

| Finance-specific exercises build readiness | Tabletop scenarios simulating payroll fraud or wire transfer compromise prepare teams for real incidents. |

The controls that most accounting teams still get wrong

The most common mistake we see at 247techify is treating insider threat prevention as either an IT problem or an HR problem. It is neither. It is a governance problem that requires both functions to operate from the same data set at the same time.

Accounting teams invest in perimeter security, endpoint protection, and annual compliance training. Then a trusted senior accountant with twelve years of tenure quietly manipulates vendor records over eight months before anyone notices. The detection gap is not a technology failure. It is a structural failure. No single system was watching the full picture.

The second oversight is underestimating how much remote work and AI-assisted finance tools have expanded the insider risk surface. Cloud-based ERP access from personal devices, AI tools that can generate synthetic invoices, and collaboration platforms that blur the line between internal and external data sharing all create new exposure points that traditional SoD controls were not designed to address.

Finance-specific tabletop exercises are the most underused readiness tool in accounting security. Most firms run generic IT incident response drills. Running a scenario where a payroll administrator’s credentials are compromised and used to redirect direct deposits forces your team to discover the gaps in their detection and response workflow before an attacker does.

The firms that handle insider incidents best are the ones that built their governance model before they needed it.

— 247techify Team

How 247techify supports insider threat prevention for accounting firms

Accounting firms and finance teams operating in regulated Canadian markets face specific compliance obligations under SOX, PCI-DSS, and PIPEDA that generic IT support cannot address.

247techify’s cybersecurity services include identity access management, continuous monitoring, and compliance auditing designed specifically for financial environments. The 247techify team provides 24/7 monitoring with a response time under 30 minutes, automated access governance reviews, and finance-specific incident response planning. With a 98% client satisfaction rate, 247techify builds insider threat prevention programs that align with your accounting operations and regulatory requirements. Contact 247techify to build a customized insider threat prevention plan for your accounting team.

FAQ

What is an insider threat in accounting?

An insider threat in accounting is any risk to sensitive financial data that originates from employees, contractors, or vendors with authorized system access. This includes negligent mistakes, deliberate fraud, and compromised credentials used by external attackers.

What types of insider threats affect financial firms most?

The three primary types are negligent insiders, malicious insiders, and compromised insiders. Negligent insiders cause 58% of incidents, making poor security practices the most common source of accounting data exposure.

How does segregation of duties prevent insider fraud?

Segregation of duties prevents any single employee from controlling an entire financial process, such as creating vendors, approving invoices, and releasing payments. Continuous automated monitoring catches accumulated access risks that periodic reviews miss.

Why do insider incidents in finance take so long to detect?

Insiders already hold legitimate access, so their activity does not trigger perimeter alerts. Detection requires behavioral baseline analysis, and without that, incidents can persist for months before causing visible damage.

How does phishing-resistant MFA reduce insider threat risk?

Phishing-resistant MFA blocks attackers from using stolen credentials to impersonate legitimate accounting staff. The FFIEC recommends MFA deployment as a baseline control for financial institutions handling sensitive transaction data.